It has long been clear that a permit is required prior to beginning actual construction of a facility that emits pollutants. However, what has not been clear and what has been the subject of much debate and interpretation over the years, is what physical activities denote or constitute the point in time when actual construction has begun.

EPA has finalized the Rescission Rule, the rescission of the greenhouse gas Endangerment Finding. EPA called it the “single largest deregulatory action in U.S. history.” Administrator Zeldin announced EPA’s intention to rescind the Endangerment Finding in March 2025 when he announced a series of sweeping deregulatory actions.

The genesis of the Endangerment Finding was an October 1999 petition for rulemaking submitted to EPA by various environmental organizations seeking regulation of greenhouse gases. The petition was based on Clean Air Action Section 202(a)(1), which states that EPA shall prescribe standards applicable to the emission of any air pollutant from new vehicles or engines “which in his judgment cause, or contribute to, air pollution which may reasonably be anticipated to endanger public health or welfare.”

The Trump Administration has signaled that it plans to expand energy production, expedite energy permitting, and ‘roll-back’ regulations and practices that impede growth. As part of this effort, Mr. Trump has named Lee Zeldin, a former GOP member of Congress, to lead the EPA. Mr. Trump has stated that Mr. Zeldin wishes to “ensure fair and swift deregulatory decisions” while maintaining “the highest environmental standards, including the cleanest air and water on the planet.’’ Further, Elon Musk and Vivek Ramaswamy, heads of the so-called Department of Government Efficiency, or DOGE, have vowed to work with the Trump Administration to use executive action “to pursue three major kinds of reform: regulatory rescissions, administrative reductions and cost savings.”

The Supreme Court’s ruling in Sackett v. EPA continues to dominate discussions regarding the scope of jurisdiction over adjacent wetlands. Now, the Corps and EPA seek to codify that ruling into the regulatory definition of ‘waters of the United States.’

In Sackett, the Supreme Court adopted Justice Scalia’s opinion in its prior Rapanos decision. It held that the Clean Water Act extends only to those wetlands that are as a practical matter indistinguishable from waters of the United States. The Corps must establish first, that the adjacent body of water constitutes ‘waters of the United States’ (i.e., a relatively permanent body of water connected to traditional interstate navigable waters) and second, that the wetland has a continuous surface connection with that water, making it difficult to determine where the water ends and the wetland begins. Sackett v. EPA, 143 S.Ct. 1322, 1341 (20243).

In March 2025, Administrator Zeldin announced that EPA will reconsider a number of regulations in order to advance various executive orders issued by President Trump and fulfill EPA’s own Powering the Great American Comeback Initiative. These efforts include the 2024 ambient air standard for particulate matter, the 2009 endangerment finding, and the scope of jurisdiction over ‘adjacent wetlands after the Supreme Court’s 2023 decision in Sackett.

In the Biden Administration, EPA lowered the National Ambient Air Quality Standard for particulate matter, the PM 2.5 NAAQS. The standard was reduced to levels that were close to background levels in some areas. EPA announced it is “revisiting” the lower standard because, among other things, the lower standard “raised serious concerns from states across the country and served as a major obstacle to permitting.”

Carbon dioxide (CO2) is used to carbonate beverages and enhance plant growth. It has also been used for decades in enhanced oil recovery, in which CO2 is injected into oil- or gas-bearing formations to help extract oil and gas. Of course, many say that CO2 causes or contributes to climate change / global warming. In 2009, EPA issued its ‘endangerment finding’ in which EPA determined that current and projected concentrations of CO2 and other greenhouse gases in the atmosphere threaten the public health and welfare of current and future generations.

The idea of capturing CO2 before it enters the atmosphere and using it or injecting it for perpetual storage, or sequestration, came about as a way to mitigate the anticipated impacts of climate change. To facilitate carbon capture, use, and storage (CCUS), Congress created the 45Q tax credit in the US Tax Code. Additionally, the Biden Administration touted CCUS as an important tool to address climate change. Even the prior Governor of Louisiana included it as a centerpiece of his climate strategy.

The scope of jurisdiction over wetlands under the Clean Water Act has long been debated and litigated. The Supreme Court and other courts have issued various rulings explaining and limiting the scope of such jurisdiction. The Corps of Engineers (Corps) and the Environmental Protection Agency (EPA), though, have not always strictly adhered to those rulings and have sought to expand their jurisdictional reach. Now, the Trump Administration seems determined to force compliance with those rulings.

On January 20, 2025, the day of the inauguration, President Trump signed Executive Order 14154, Unleashing American Energy. Through the EO, President Trump seeks to “encourage energy exploration and production on Federal lands and waters … in order to meet the needs of our citizens and solidify the United States as a global energy leader long into the future.” He ordered an immediate review of “all existing regulations … and any other agency actions … to identify those agency actions that impose an undue burden on the identification, development, or use of domestic energy resources.” He further ordered that agencies must “expedite permitting approvals” to achieve this overall goal.

The relevant federal agencies have heard the call. Doug Burgum, the Secretary of the Interior, issued Order No. 3418 to implement the EO. In it, Secretary Burgum ordered steps be taken to reduce “barriers to the use of Federal lands for energy development” and that leases cancelled during the Biden Administration be reinstated. Chris Wright, the Secretary of the Department of Energy, criticized net-zero policies, stating that they threaten the reliability of our energy system and achieve “precious little in reducing global greenhouse gas emissions.” He resumed consideration of pending applications to export American liquefied natural gas (LNG). Towards that end, he announced a new export authorization for the Commonwealth LNG project proposed for Cameron Parish, Louisiana and provided an export permit extension for Golden Pass LNG Terminal, currently under construction in Sabine Pass, Texas

EPA is also involved. Administrator Zeldin announced an initiative, titled Powering the Great American Comeback, which included his ‘five pillars’ approach. The ‘pillars’ include Restoring American Energy Dominance and Permitting Reform, Cooperative Federalism, and Cross-Agency Partnership. Energy produced in America “is far cleaner than energy produced overseas” and is better for the environment because “we do it better here.” However, the cost and length of time to obtain necessary permits is a potential impediment to achieving these goals. EPA will “bring down that timeline [to] make sure it doesn’t take as long to get a permit.”

Administrator Zeldin also announced that EPA will reconsider over thirty regulations. These include the standards of performance for oil and gas facilities (Subparts OOOOb/c) and the effluent limitations guidelines and standards (ELGs) for wastewater discharges for oil and gas extraction facilities. EPA will also reconsider regulations on power plants (the Clean Power Plan 2.0).

Overall, though, perhaps the most important one is the reconsideration of the 2009 Endangerment Finding and all of the regulations and actions that rely on it. In the Endangerment Finding, EPA concluded that carbon dioxide (CO2), methane (CH4), and other greenhouse gases threaten public health and welfare. While the Finding itself did not impose any requirements, it was a “prerequisite for implementing greenhouse gas emissions standards for vehicles and other sectors.” Secretary Wright stated that the Finding “has had an enormously negative impact on the lives of the American people. For more than 15 years, the U.S. government used the finding to pursue an onslaught of costly regulations – raising prices and reducing reliability and choice on everything from vehicles to electricity and more.”

In addition to its regulatory impact, EPA provided other reasons for the reconsideration. First, when EPA announced the Finding, it indicated that, by itself, it did not impose any costs and that EPA could not consider future costs when making the Finding. However, EPA has subsequently relied on the Finding as part of its justification for certain regulations with an aggregate cost of more than one trillion dollars. Second, the Finding itself acknowledged significant uncertainties in the science and assumptions used to justify the decision but EPA has never sought comment on major developments in innovative technologies, science, economics, and mitigation that may impact the Finding. Finally, major Supreme Court decisions, including Loper Bright Enterprises v. Raimondo, have provided new guidance on how EPA should interpret statutes to discern Congressional intent and ensure that its regulations follow the law.

EPA, and the other federal agencies reviewing their existing regulations and prior actions to implement the EO, must exercise some caution in changing policies. In very general terms, an agency must indicate an awareness that it is changing position, show that the new policy is permissible under the statute, indicate that the new policy is better, and provide reasons for adoption of the new policy. In light of Loper Bright, an agency would likely have to show that the new policy is not just permissible but in line with the ‘best reading’ of the statute. Overall, the agency must provide a reasoned explanation for the change. They must also follow the Administrative Procedure Act. To amend or revoke a rule, notice and comment are required and decisions are subject to judicial review. The reconsideration process will take some time and the outcome is not at all certain due to the ongoing threat of litigation.

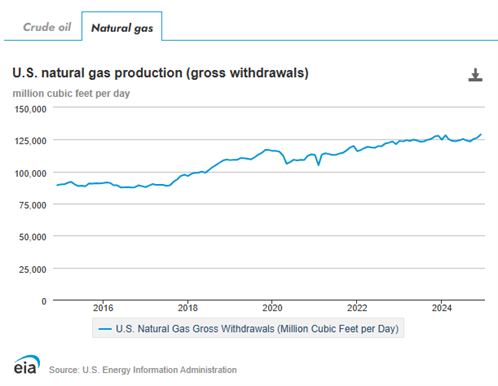

An increased emphasis on the domestic production of oil and gas and a decline in regulatory burdens are certainly welcome to the oil and gas industry and those related industries that depend on fossil fuels. Oil and gas production, which is higher now than at the start of the pandemic (see figures below), can only reach new heights.